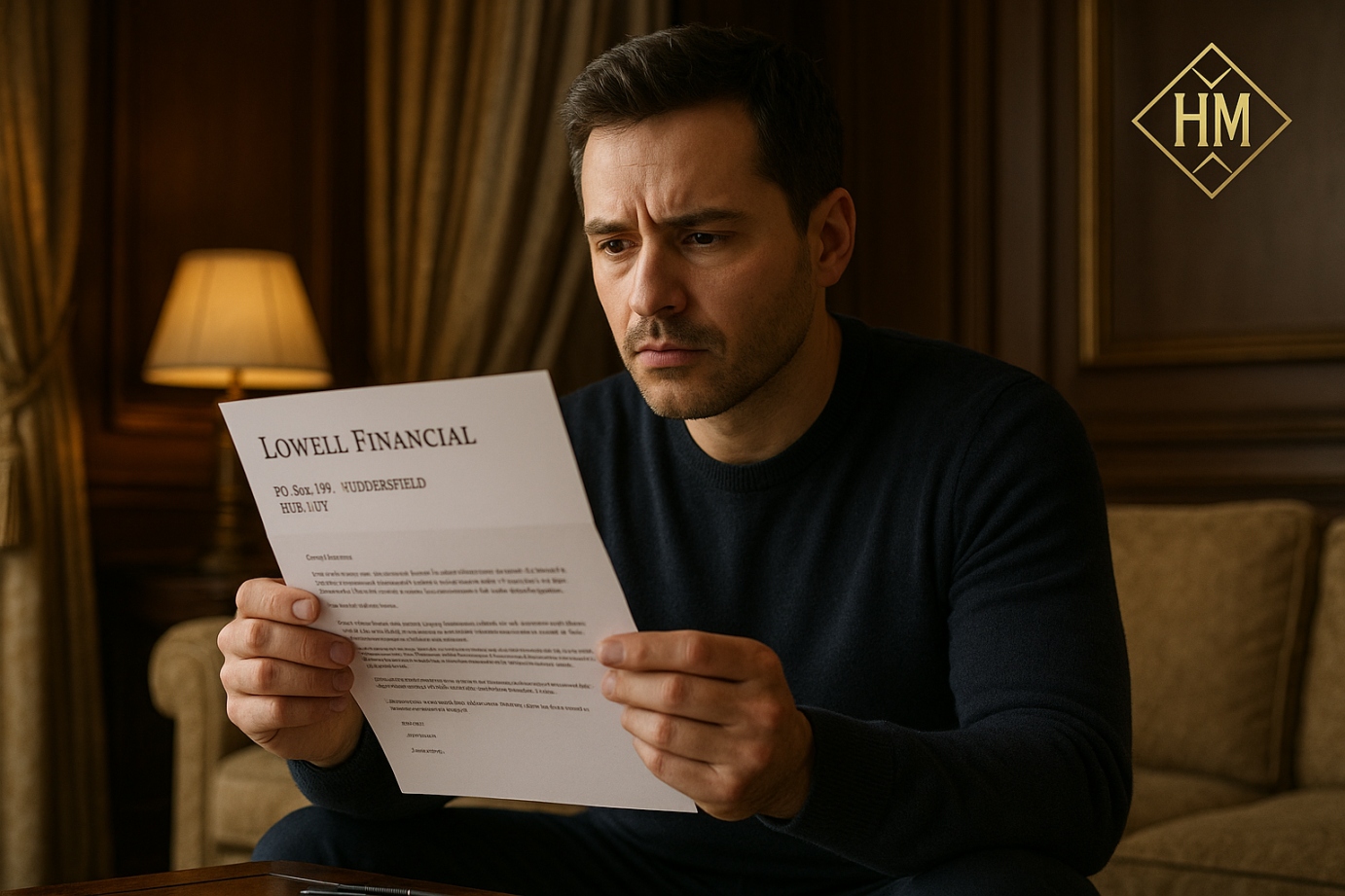

Receiving a letter from po box 189 huddersfield hd8 1dy can be a stressful experience. This address is associated with Lowell Financial Ltd, a debt collection and debt purchasing company operating in the UK. Letters from Lowell can be intimidating because they involve claims about money owed, possible legal actions, and the fear of harassment. This guide provides a full explanation of what the letters mean, your rights, and practical steps you can take to handle them effectively.

Who is Lowell Financial?

Lowell Financial Ltd is a UK-based company that specializes in collecting overdue debts and purchasing debts from creditors such as banks, credit card companies, and utility providers. When a debt is sold to Lowell, the responsibility for collection shifts from the original lender to the agency, but the total debt owed by the consumer remains the same.

Lowell operates under strict regulatory requirements. They are expected to treat consumers fairly, avoid harassment, and follow ethical debt collection practices. Despite the reputation that debt collectors can be aggressive, Lowell also provides guidance on budgeting and repayment, helping consumers manage their financial obligations responsibly.

Why You Might Receive a Letter from po box 189 huddersfield hd8 1dy

Receiving correspondence from Lowell does not always mean you owe money. There are several reasons why a letter might arrive:

-

Debt Collection: Lowell may have purchased a debt that you owe from an original creditor. The total amount due remains the same, but Lowell now manages collection.

-

Verification of Information: The agency may need to confirm your identity or account details to ensure that the debt records are accurate.

-

Payment Proposals: Lowell may suggest a repayment plan or settlement option based on your financial situation.

-

Legal Threats: If a debt is ignored, Lowell may escalate the matter with warnings about legal proceedings, including court actions.

-

Mistaken or Disputed Debts: Occasionally, a debt may be incorrectly assigned to someone. Verification is crucial before taking action.

Your Rights When Contacted by Lowell

Understanding your rights helps you handle debt letters confidently.

Requesting Proof of Debt

You are entitled to request documentation proving that the debt is valid and that Lowell has the right to collect it. This includes:

-

A copy of the original credit or loan agreement.

-

A detailed statement showing interest, charges, and payments.

-

Documentation confirming that Lowell legally owns the debt.

This process ensures you are not paying a debt that is not yours.

Protection Against Harassment

Debt collectors must not harass or intimidate you. Harassment includes repeated calls, threats, or pressure to pay more than you can afford. You have the right to document all communications and report unfair behavior if it occurs.

Statute-Barred Debt

In the UK, some debts can become unenforceable after six years (five years in Scotland) if there has been no acknowledgment or payment. These debts are considered statute-barred, meaning they cannot be legally enforced through the courts. However, collectors may still contact you, so it’s important to know your rights and avoid making payments that could reset the limitation period.

Filing Complaints

If Lowell’s conduct is inappropriate or aggressive, you can file a formal complaint directly with the company. If unsatisfied with the response, you may escalate to independent review processes to ensure your rights are protected.

Step-by-Step Guide to Handling a Lowell Letter

Step 1: Stay Calm and Review

Carefully read the letter. Note:

-

The debt amount claimed.

-

The original creditor.

-

Reference numbers and account details.

-

Proposed payment amounts or deadlines.

Step 2: Request Proof of Debt

Send a formal request for validation. Ask for:

-

A detailed breakdown of the debt.

-

A copy of the original agreement.

-

Evidence that Lowell has legal authority to collect.

-

Information about the original creditor.

Keep copies and send the letter via recorded delivery.

Step 3: Check Your Credit Report

Review your credit report to confirm the debt exists and matches Lowell’s claim. Check the default date and payment history. This helps you determine if the debt may be statute-barred.

Step 4: Determine Statute-Barred Status

Use your records to calculate when the last payment or acknowledgment occurred. If the required period has passed without activity, the debt may be statute-barred, limiting Lowell’s ability to take legal action.

Step 5: Negotiate Payment Plans

-

Determine what you can afford.

-

Propose a structured payment plan to Lowell.

-

Consider a full-and-final settlement if you can make a lump-sum payment.

-

Adjust your plan if your financial situation changes.

Step 6: Seek Independent Advice

Professional debt advice can help:

-

Evaluate repayment options.

-

Prepare letters and communications.

-

Explore alternative solutions like formal debt arrangements or consolidation if needed.

Step 7: Manage Harassment

If Lowell contacts you excessively:

-

Document all calls, letters, and messages.

-

Send a complaint outlining unacceptable behavior.

-

Specify preferred communication methods.

-

Escalate unresolved issues to independent review processes.

Step 8: Prepare for Legal Action

Lowell may escalate to court if debts are ignored. In such cases:

-

Respond promptly to court documents.

-

Consider legal or professional advice.

-

Determine if a statute-barred defense applies.

-

Maintain detailed records of all communications.

Common Concerns and Misconceptions

-

Scams and Fraudulent Letters: Always verify authenticity before providing personal information.

-

Aggressive Contact: You are protected against harassment and can file complaints.

-

Old Debts: Statute-barred debts may limit legal enforcement.

-

Financial Hardship: Negotiating affordable repayment plans or settlements is possible.

-

Collector Misconduct: Escalate complaints if rules are broken.

Practical Tips for Dealing with Lowell Financial

-

Prefer written communication over phone calls.

-

Keep copies of all letters and proof of postage.

-

Avoid ignoring the debt — taking proactive steps gives you control.

-

Do not borrow additional money unnecessarily to pay.

-

Take care of your mental health — financial stress can be overwhelming, and support is important.

Sample Debt Validation Letter

Conclusion po box 189 huddersfield hd8 1dy

A letter from po box 189 huddersfield hd8 1dy (Lowell Financial) can feel intimidating, but understanding the process and your rights empowers you to act. Key points to remember:

-

Remain calm and read the letter carefully.

-

Request proof before making any payment.

-

Know that harassment is not allowed.

-

Verify the debt with your credit report.

-

Negotiate payments based on your ability.

-

Seek professional debt advice when needed.

-

Keep records of all correspondence and communications.

-

Escalate complaints or legal concerns appropriately.

-

Prepare carefully if court action is threatened.

-

Take care of your mental well-being throughout the process.

By following these steps, you can navigate debt collection effectively, protect your rights, and take practical steps toward resolving financial obligations.

I Liked This Topic: Marciemcd25

[…] Also Read This Topic: PO Box 189 Huddersfield HD8 1DY […]